Statistics on Interest Rates applied by Monetary Financial Institutions

The Central Bank of Cyprus has today released the statistics on the average interest rates1 applied by monetary financial institutions (MFIs) in Cyprus on deposits and loans of euro area residents in euro, as well as data regarding volumes (amounts) of new euro denominated loans to euro area residents for the reference month of January 2026. These statistics are included in the February 2026 edition of Monetary and Financial Statistics. In parallel, comparative data for the eurozone countries are presented in the Data Portal of the European Central Bank.

The main developments in interest rates on new deposit and loan contracts, including contracts which were renegotiated, are summarized as follows:

Deposit Rates

- The interest rate on deposits from households with an agreed maturity of up to one year remained unchanged at 1,20%, compared with the previous month.

- The corresponding interest rate on deposits from non-financial corporations registered an increase to 1,34%, compared with 1,27% in the previous month.

Lending Rates2

- The interest rate on consumer credit decreased to 7,20%, compared with 7,22% in the previous month.

- The interest rate on loans for house purchase decreased to 3,70%, compared with 3,78% in the previous month. It is noted that, the portfolio of loans for house purchase of the MFIs contains various types of loans, such as loans for primary residence, for vacation houses etc, which bear different risk and interest rate. The composition of the housing loans portfolio varies from month to month, resulting in changes to the level of the weighted average interest rate, independently of the increases or decreases of the interest rates of the MFIs.

- The interest rate on loans to non-financial corporations for amounts up to €1 million remained unchanged at 4,32%, compared with the previous month. The interest rate on loans to non-financial corporations for amounts over €1 million registered a decrease to 4,34%, compared with 4,42% in the previous month.

Amounts of pure new loans3

Pure new loans recorded a decrease to €247,3 million in January 2026 (from total of €495,9 million), compared with €625,0 million (from total of €986,9 million) in the previous month. The main categories of new loans are analysed below:

- Pure new loans for consumption increased to €18,9 million (from total of €20,1 million), compared with €17,2 million in the previous month (from total of €18,2 million).

- Pure new loans for house purchase recorded a decrease to €95,7 million (from total of €138,1 million), compared with €135,4 million in the previous month (from total of €178,1 million).

- Pure new loans to non-financial corporations for amounts up to €1 million decreased to €40,1 million (from total of €53,1 million), compared with €60,3 million in the previous month (from total of €92,5 million).

- Pure new loans to non-financial corporations for amounts over €1 million registered a decrease to €88,1 million (from total of €277,2 million), compared with €406,4 million in the previous month (from total of €685,0 million).

Cyprus interest rates in a European context: Analysis and comparison

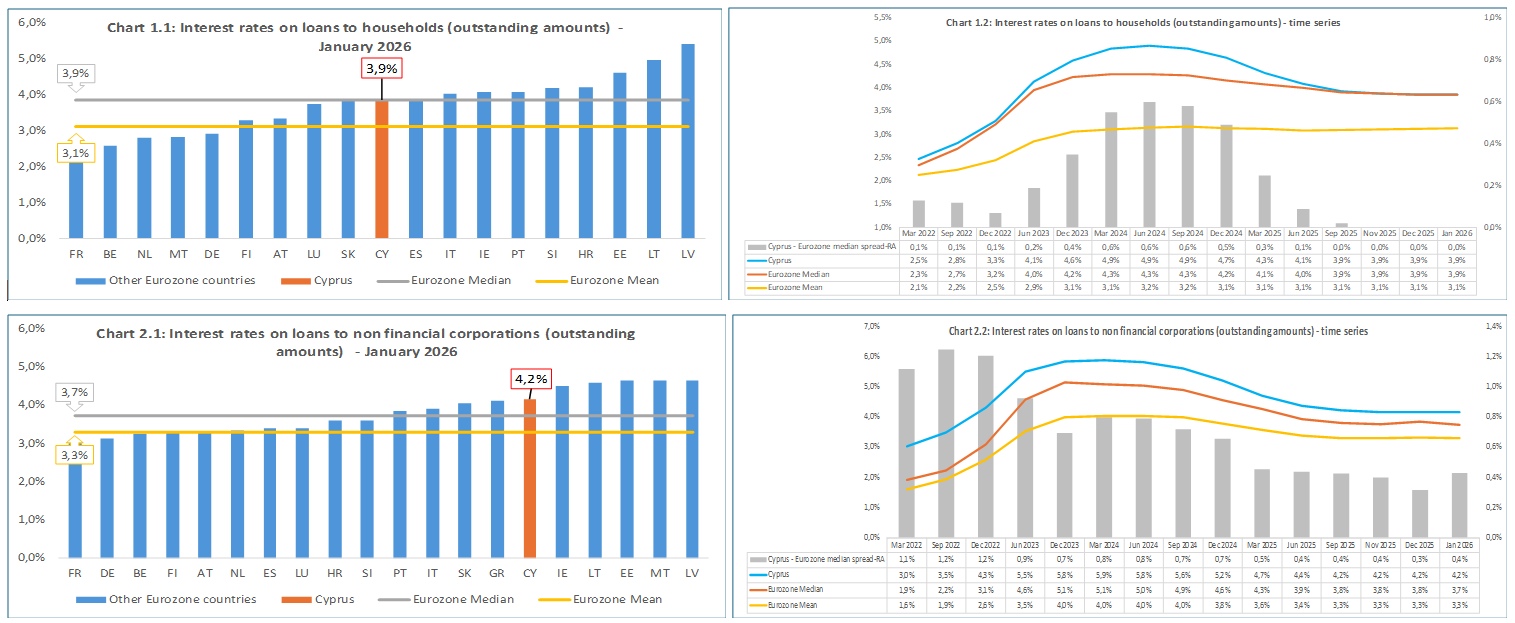

Loan interest rates (outstanding amounts)

The interest rate level on outstanding loans in Cyprus is close to the respective Eurozone median4, with the spread standing at zero (0,0%) for households (charts 1.1 and 1.2) and to 0,4% for non-financial corporations (charts 2.1 and 2.2).

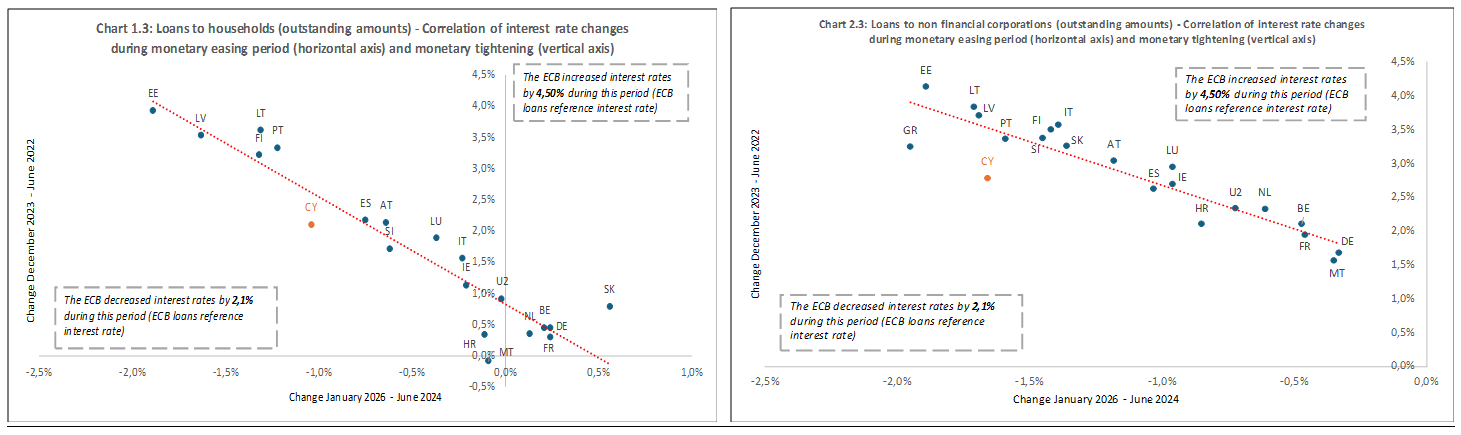

The correlation between the transmission rates of monetary easing (horizontal axis) and monetary tightening (vertical axis) in Cyprus, is in line with the other Eurozone countries in outstanding loans, both to households and non-financial corporations. More specifically, the correlation between the decrease observed in loans interest rates during the monetary easing period (i.e. for the period June 2024 – January 2026), with the respective increase during the monetary tightening period (i.e. for the period June 2022 – December 2023), is favourably compared with the other Eurozone countries (charts 1.3 and 2.3)

Loan interest rates (new business)

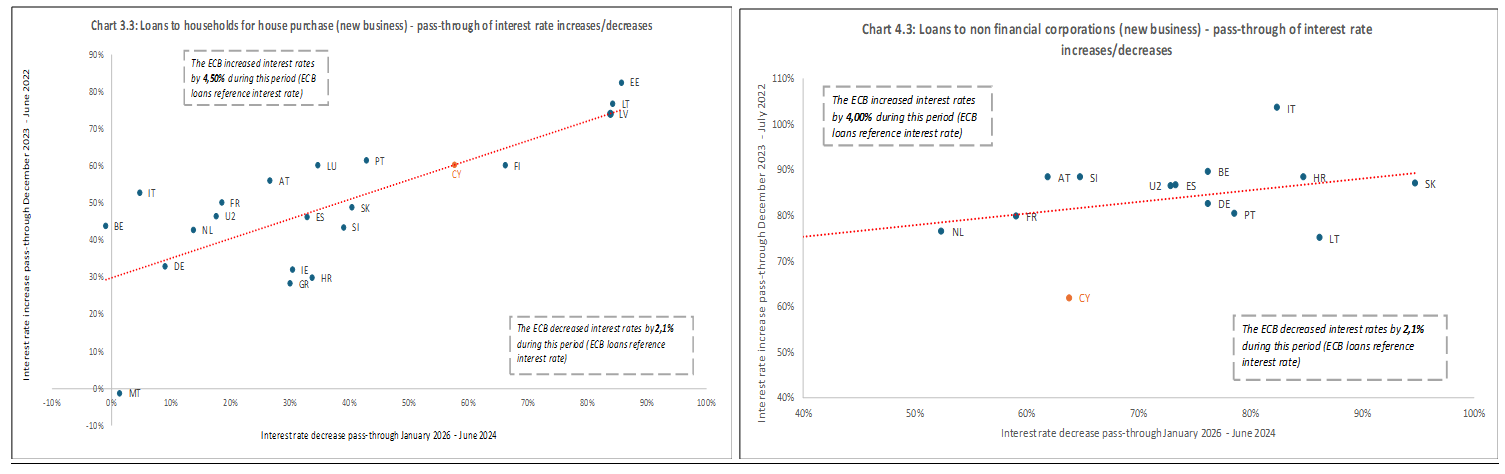

The interest rate level on new loans in Cyprus is comparable to the Eurozone median. More specifically, the spread between the weighted average interest rate on loans to households for house purchase stands at -0,3% (lower than the Eurozone median), (charts 3.1 and 3.2), while the respective spread for non-financial corporations stands at 0,5% (charts 4.1 and 4.2).

The correlation between the pass – through of the transmission rates of monetary easing (horizontal axis) and monetary tightening (vertical axis) in Cyprus, is in line with the other Eurozone countries in new loans to households for house purchase. In relation to new loans to non-financial corporations, the pass – through in Cyprus appears to be weaker, both during the monetary tightening period (increase of interest rates) and the monetary easing period (decrease of interest rates). However, it is it is observed that the average pass – through rate in Eurozone during the monetary tightening period (increase of interest rates) was higher than the respective pass – through rate during the monetary easing period (decrease of interest rates) in loans to households for house purchase and loans to non-financial corporations, by 29% and 14% respectively. The pass – through rate for households in Cyprus during the monetary tightening period was by only 2,6% higher than the respective pass – through rate during the monetary easing period, while for non-financial corporations it was by 2% lower (charts 3.3 and 4.3).

Deposit interest rates (outstanding amounts)

In contrast to the loans interest rates, interest rates on outstanding deposits in Cyprus are considered as outlier, standing at the lower level within Eurozone (charts 5.1 to 6.2). This might be attributed to the excess liquidity of credit institutions in Cyprus, which is among the higher ones within Eurozone. (indicatively, the Liquidity Coverage Ratio – LCR in Cyprus in December 2025 stood at 319%, compared with 192% (median) and 161% (mean) in European Union in September 2025), as well as to the short range of the banking sector in Cyprus.

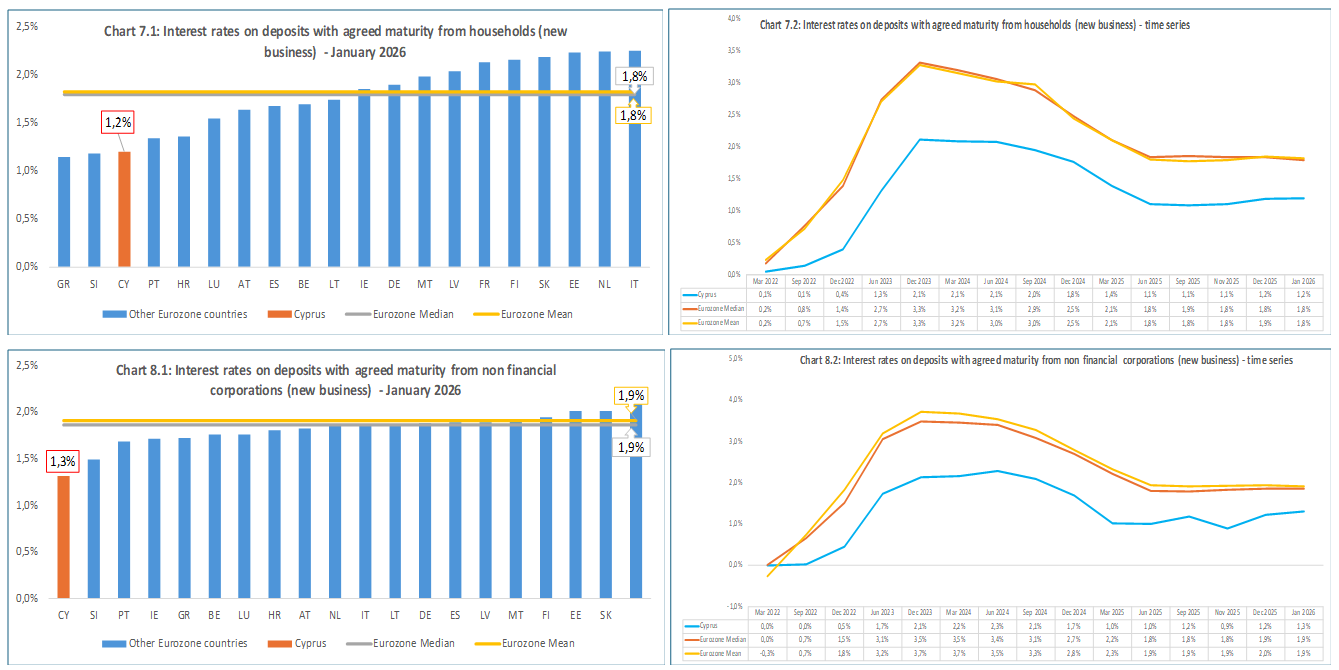

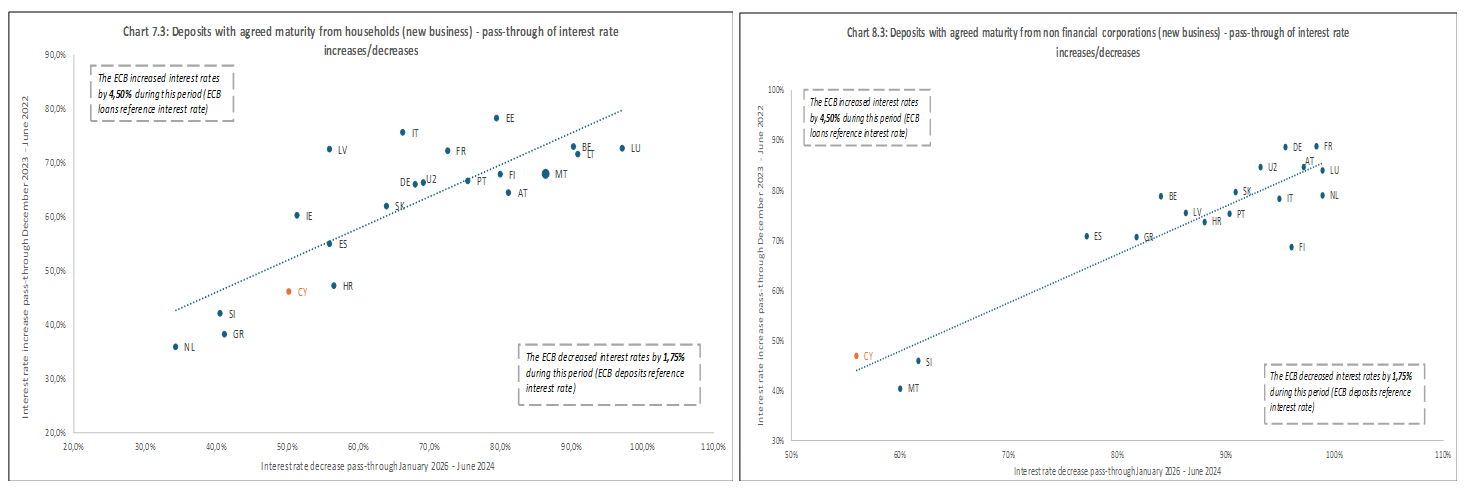

Deposit interest rates (new business)

The interest rates on new deposits in Cyprus are standing at similar levels with interest rates on outstanding deposits (charts 7.1 to 8.2), due to the same reasons mentioned above.

The pass – through of increases and decreases of interest rates in deposits in Cyprus appears to be weak as compared with almost all other Eurozone countries, both for households and non-financial corporations. It is observed that the average pass – through rate in Eurozone during the monetary tightening period (increase of interest rates) was lower than during the monetary easing period (decrease of interest rates) in the new deposits portfolio of households and non-financial corporations, by 1,2% and 6,2% respectively. The respective differences between the pass – through rates are slightly higher in Cyprus and they stand at 5% and 14% for households and non-financial corporations respectively (charts 7.3 and 8.3).

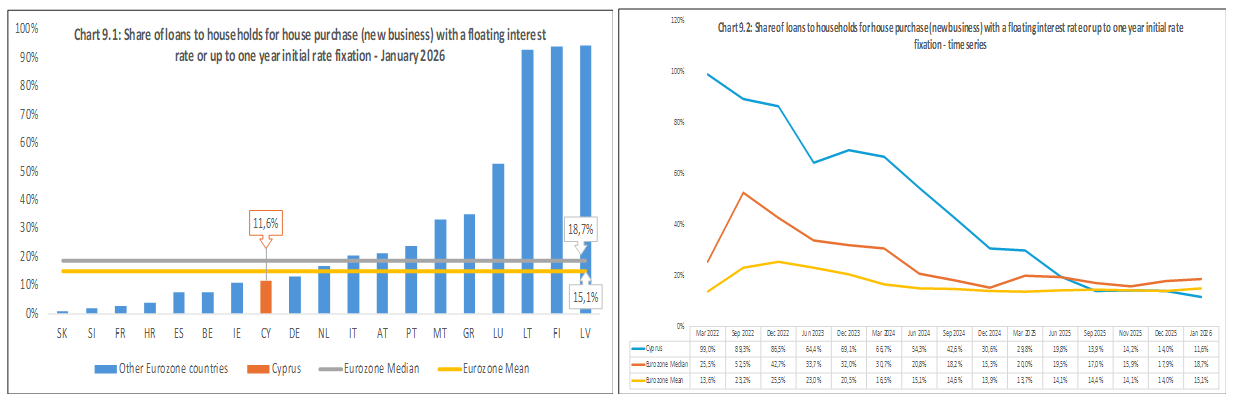

Type of interest rate of loans to households for house purchase

The share of new loans tο households for house purchase with variable interest rate is aligned with the Eurozone. The said share follows a sharply declining trend in recent years. From almost 100% at the beginning of 2022, it has fallen to 11,6% today, which is lower than the Eurozone median (charts 9.1 and 9.2). This may be partly affected by the choice of fixed-rate lending in the early years (e.g. 3-5 years), and their subsequent conversion to a floating rate. Consequently, there is a change in the behaviour of borrowers regarding interest rate risk, an element that should be taken into account in banks' risk management policies.

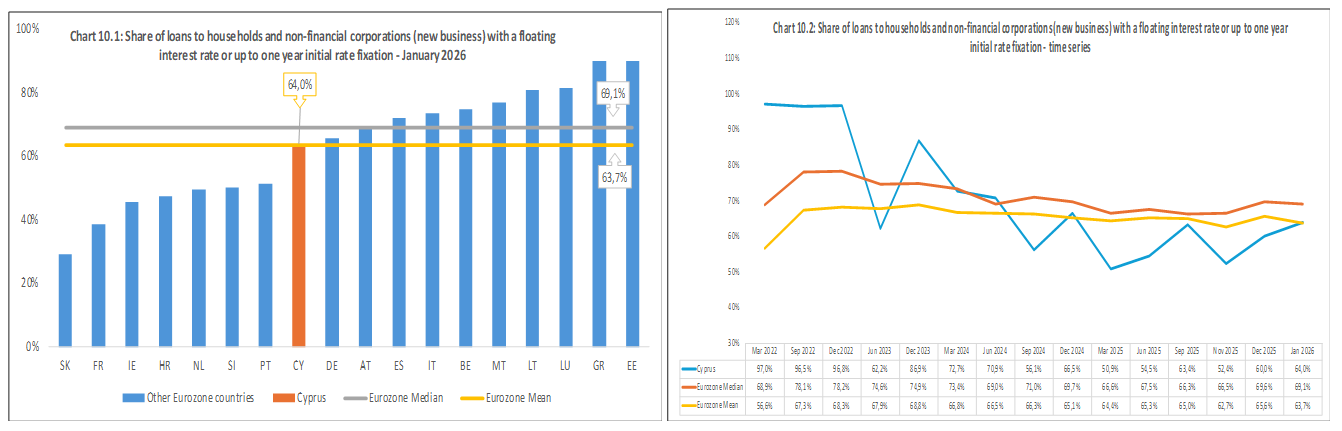

Type of interest rate of loans to households and non financial corporations

The share of new loans to households and non-financial corporations with floating interest rate compares favourably with the Eurozone. The said share follows a declining trend in recent years. From almost 100% at the beginning of 2022, it has fallen to 64% today, which is lower than the Eurozone median (charts 10.1 and 10.2). This may be partly affected by the same reason mentioned above and should be taken into account in banks' risk management policies.

Click here.

- In accordance with the provisions of Regulation 2013/34, as amended, of the European Central Bank, interest rates are calculated as weighted average interest rates, which are sensitive to outliers.

- Lending rates refer to loans with floating interest rate and up to one year initial rate fixation.

- Amounts of pure new loans include only new loan contracts. Total new loans include new loan contracts and contracts which were renegotiated within the reference month.

- For the purposes of this analysis, the median is considered as a more appropriate measure of comparison, since it is not sensitive to outliers mainly arising from countries with large portfolios. Several countries might not appear on some charts, since their data is not published on the ECB data portal, for statistical confidentiality purposes.